Something odd happened this week. Actually, four things happened. And I don't think they're unrelated.

On June 1, Anthropic confidentially filed its S-1 with the SEC. The same day, GitHub Copilot switched every developer to metered token billing. By June 5, Broadcom issued a weak forecast and half a trillion dollars evaporated from AI stocks in a single session. Two days later, the Financial Times reported that OpenAI executives are telling employees "chat is dead" while racing to rebuild ChatGPT as a super-app before their own IPO.

I don't think any of this is random noise. I think it's the same story, seen from four angles.

Anthropic went from $61B to $965B in 14 months

Let that number sit for a second. Fourteen months ago, Anthropic was valued at $61.5 billion. Last week, it closed a $65 billion Series H at a $965 billion post-money valuation.

That's a 15.7x multiple in just over a year, across four funding rounds that got progressively larger and faster: $3.5B Series E in March 2025, $13B Series F by September, $30B Series G in February 2026, and then the $65B whopper on May 28. Lightspeed, ICONIQ, GIC, Coatue, Altimeter, Dragoneer, Greenoaks, Sequoia. Every major institutional name you can think of has a piece of this.

The revenue story sounds incredible on paper: a $47 billion annualized run rate, up from about $10 billion last year. But here's what I keep wondering: how much of that is real, durable enterprise adoption, and how much is what people are now calling "tokenmaxxing"?

Tokenmaxxing is the polite term for what happens when companies hand out AI tools to every employee and say "use it as much as possible" without measuring whether any of it actually helps. It burns through tokens at an absurd rate. It inflates the revenue numbers of every model provider. And it's already starting to reverse.

Uber's COO just admitted they're not seeing proportional productivity gains from rising AI costs. Starbucks shut down an AI inventory experiment because the model couldn't be trusted. Microsoft reportedly cut off Claude Code licenses partly over costs. The Financial Times crunched the ROI numbers: Microsoft at negative 9 percent, Google at negative 15, Meta at negative 28, Oracle at negative 35. Only Amazon barely broke positive.

That's not a growth story. That's a subsidized consumption bubble that's starting to leak.

SpaceX is going public today at $1.77 trillion

As I write this, SpaceX is debuting on the Nasdaq at $135 a share under the ticker SPCX, raising $75 billion. It's the largest IPO in history by a wide margin. Saudi Aramco's $29 billion raise in 2019 looks modest by comparison.

The company did $18.67 billion in revenue in 2025, which means it's trading at roughly 95 times sales. For context, even during peak dot-com mania, the most aggressive comps rarely crossed 30x or 40x revenue. This is different territory.

What makes it relevant to the AI story is the xAI merger. In February, Musk folded xAI into SpaceX in an all-stock deal that valued the AI unit at roughly $80 billion. xAI's financials are genuinely staggering: $6.355 billion in operating losses in 2025, on pace to burn about $10 billion this year. The Colossus 1 data center in Memphis houses 220,000 Nvidia GPUs across 300 megawatts of power and was reportedly built in 120 days. That's genuinely impressive engineering. It's also a money furnace.

Then there's the Anthropic compute deal: $1.25 billion per month through May 2029. That's roughly $40 billion over the life of the contract, though either party can walk with 90 days' notice. When your biggest customer contract also involves paying your biggest competitor for compute, the web gets very tangled very fast.

OpenAI says chat is dead

This one is wild to me. The product that made OpenAI the face of the AI revolution (the chat interface that everyone from college students to Fortune 500 CEOs now recognizes), and a senior employee told the FT flatly: "Chat is dead."

Chief product officer Thibault Sottiaux described the vision as a unified super-app where "you have your own personal agent that is capable of helping you across everything in your life, be it personally or at work." The revamp hits ChatGPT's web and mobile apps in the coming weeks. ChatGPT, Codex, and other product teams have already been merged under Sottiaux.

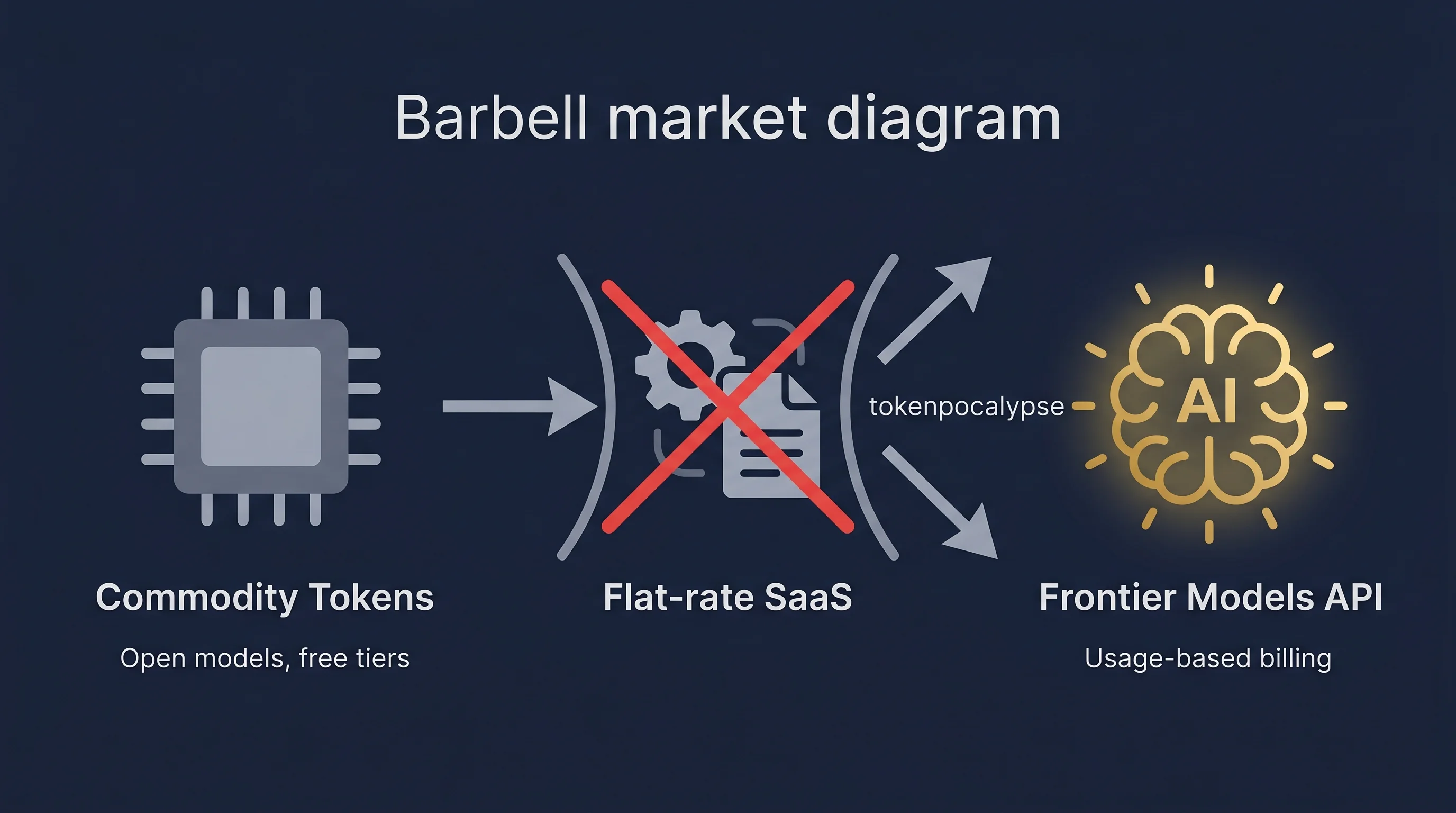

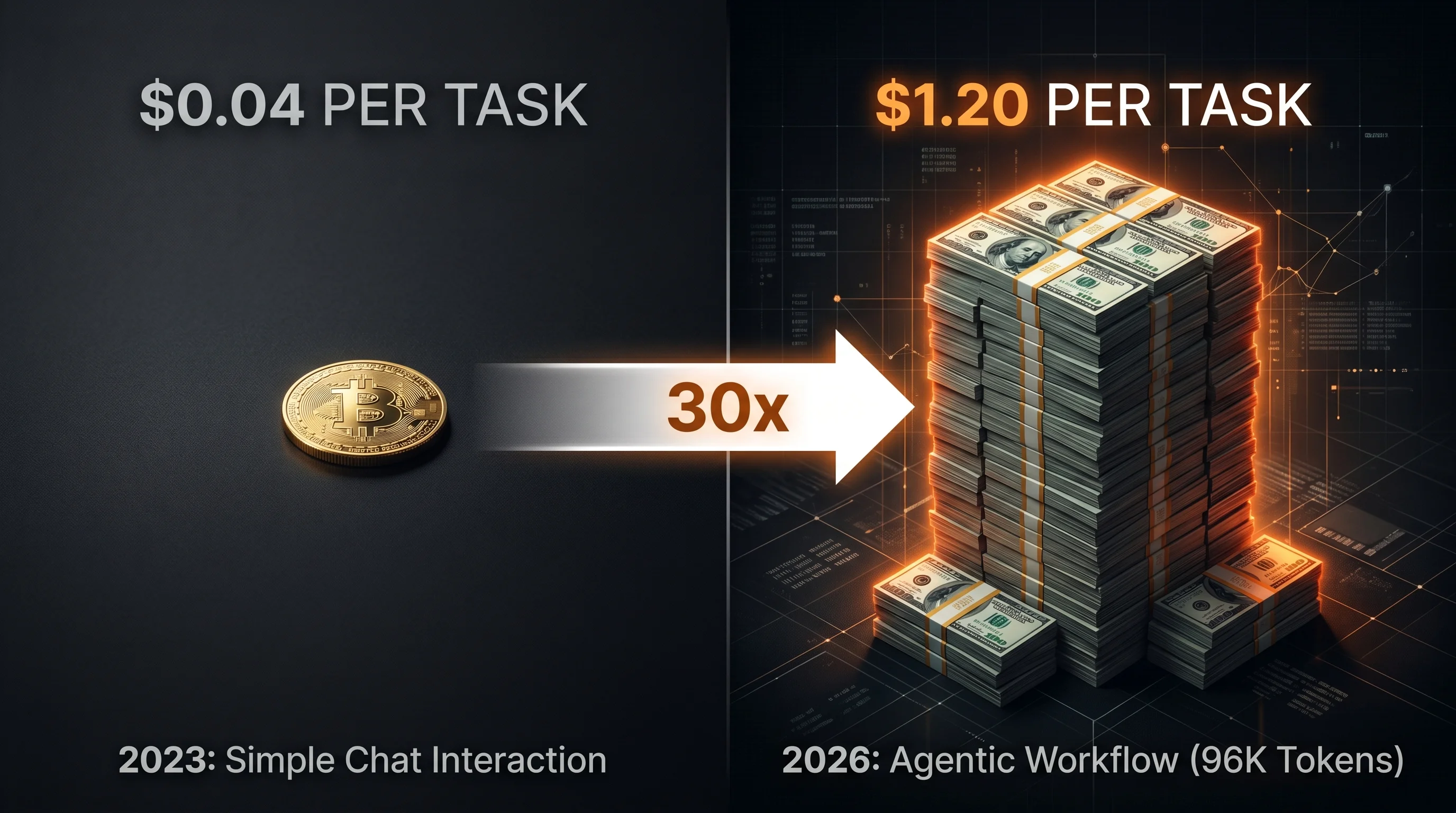

The subtext here is hard to miss. OpenAI is racing toward its own IPO and needs a revenue story that goes beyond $20-a-month subscriptions. Chat doesn't monetize well enough. Agents that autonomously burn through 96,000 tokens per task (more text than the entire novel The Great Gatsby). That's where the unit economics work out for the provider.

The irony is thick. Per-token prices have fallen 98 percent since late 2022. But enterprise AI bills have risen an estimated 320 percent over the same period. Cheaper per unit. Catastrophically more expensive overall. A simple linear AI interaction in 2023 cost roughly $0.04. An agentic workflow in 2026 costs about $1.20 per task. Per-developer consumption at enterprise companies is up 18.6x in nine months.

The models got cheaper. We just started using them 30 times more.

The tokenpocalypse is real

GitHub Copilot's billing change on June 1 crystallized what's happening across the industry. The headline prices didn't change: Copilot Pro is still $10 a month, Business is still $19 per user. But the meter underneath is now metered. Once you exhaust the included monthly credits, every model call is billed at per-token rates.

Within 48 hours, developers started comparing bills. One Redditor reported a jump from $29 to $750 a month. Another from $50 to $3,000. Some users with light workflows saw no change. The variance is the story: your bill now depends entirely on how you use the tool, and most developers had no idea what their usage profile looked like.

Anthropic made the same move. By March 2026, the legacy flat-fee enterprise plan was gone. New customers pay a $20 base per user per month, with all usage billed at standard API rates on top. One European company reported their projected monthly cost jumping from roughly €67 to €966.

And here's the thing: GitHub specifically removed the fallback to a lower-cost model when your quota runs out. If you want to keep using the tool the same way after hitting the cap, you pay the premium rate on the premium model. There is no budget option. It's the single most aggressive design choice in any of these pricing changes. It tells you exactly how much pressure these companies are under to turn subsidized users into paying customers before the IPO window opens.

Gary Marcus called it AI's Black Friday

On June 5, Broadcom posted a disappointing earnings forecast. The selloff that followed wiped roughly half a trillion dollars from AI-related stocks in a single session. Nvidia, Broadcom, Micron, CoreWeave, Nebius, Oracle, Microsoft, Meta. All took hits significantly larger than the broader market.

Marcus, who's been arguing the generative AI economics don't work for years, titled his post "AI's Black Friday" and predicted that calls for government bailouts are coming. His argument, stripped down: the circular financing that propped up the industry is unraveling, the enterprise ROI numbers are negative across the board, and once retail investors and index funds are holding the bag, "too big to fail" becomes the next narrative.

The Nvidia-OpenAI circular deal tells you everything about how fragile this structure is. Nvidia was reportedly going to invest $100 billion into OpenAI, which would then use most of that money to buy Nvidia chips. The money would basically travel in a circle, inflating both companies' numbers without creating new value. That deal has reportedly been pulled back to something closer to $20 billion. When a $100 billion "investment" between two of the most important players in the ecosystem evaporates over a weekend, the word "unsettling" doesn't quite cover it.

I'm not saying Marcus is right about everything. He's been wrong about timelines before. But when Broadcom, Uber, Starbucks, and Microsoft are all signaling the same thing at the same time (that AI costs are running ahead of AI value), it stops being a theory and starts being data.

What I actually think

I don't have a clean conclusion here. I think AI is genuinely useful for a lot of things. I use Claude every day. I ship features faster with Copilot than without it. The technology works, in ways that matter.

But I also think the capital markets have gotten far ahead of the actual economics. Three companies that have never been profitable, two of which haven't even disclosed audited financials, are collectively trying to raise or float at valuations approaching $4 trillion. Index funds, the backbone of most people's retirement accounts, will be forced to absorb these positions whether the fundamentals support them or not.

The tokenpocalypse isn't a bug. It's the moment the subsidies end and the real cost of running these models at scale gets passed to the people actually using them. If the productivity gains were real and measurable and widespread, that would be a non-issue. Companies would pay the higher bills without blinking because the ROI would justify it.

The fact that companies are already pulling back (cutting licenses, questioning agent budgets, admitting they can't see the productivity lift), that's the signal I'm watching most closely.

I don't know if this is a bubble that pops next month or something that unwinds slowly over two years. But I do know that a $965 billion valuation on a company that has never filed a public income statement, in a market where enterprise customers are already signaling cost fatigue, feels like the kind of thing that future business school case studies are written about.

What do you think? Are we in a bubble, or am I just looking at the wrong numbers?